Introduction

Digital banking services are now of critical importance to financial services customers. In the digital age we live in, banks must be able to offer complex products whilst giving customers access to services at their fingertips. Many of the ‘analogue’, traditional

banks have been slow to change the way they prioritise business cases to compete with the ‘digital’, challenger banks.

In this article, I evaluate the differences between business case evaluation in traditional banks and challenger banks. I also explore how financial institutions can strengthen relationships with key fin-tech providers by prioritising certain business cases.

Evidence includes first-hand experience from Be | Shaping the Future UK’s (Be UK) consulting practice, supplemented by anecdotal use-cases from changes publicised by leading financial institutions in the UK.

An Overview of Business Cases

Banks have realised that, in the digital era we are living in, they must focus on developing digitalisation strategies. Once the strategy has been defined, business cases must be built for each project to support the banks’ new objectives. However, many

of the ‘analogue’, traditional banks have been slow to change the way they prioritise business cases.

Established financial services institutions have already recognised the need to change project delivery methodologies to enable them to compete more effectively with the digitally savvy challenger banks. Well publicised ‘transitions from Waterfall to Agile’

have helped banks deliver functionality faster via ‘minimum viable products’. This has helped traditional banks vastly improve their online account opening processes and on-going account management is mostly digital. Traditional banks’ are making steps in

the right direction, but to truly compete with the challenger banks, traditional banks’ must start to compete on all fronts. They can do this by changing their business case evaluation process.

Traditional Banks’ Evaluation Methodologies

Historically, business cases in the banking sector have been prioritised using scoring methodologies that consider the following factors:

- Will the project increase revenue or reduce costs?

- Will the project deliver a regulatory requirement?

- Will the project significantly improve customer service or reduce operational risk?

- Is the project sponsored by a senior stakeholder?

The rationale behind each of these questions is clear: they focus on profit; whilst reducing reputational risk and allowing trusted, senior members of the bank to prioritise projects that are strategically important to each business area.

These factors have been successful in driving traditional banks business cases and are still relevant in the digital era. For example, the Coronavirus pandemic has led to a huge increase in the percentage of the population that work from home. The Bank of

England has shown that approximately 20% of people in the UK now work from home full-time, up from 5% before the pandemic(1). Therefore, senior leadership will be more likely to sponsor a project to reduce office space as this will help control costs (and

reduce their carbon footprint – helping to achieve a ‘net zero’ carbon strategy (or similar)). The strength of the historic business case evaluation methodology is that it focuses on the measurement of direct benefits to the traditional bank.

Challenger Banks’ Evaluation Methodologies

Challenger banks are pioneering new ways of evaluating business cases. They are focusing on criterion that garner ‘indirect’ benefits. These positive externalities include factors such as ‘word-of-mouth’ advertising or ‘search engine optimisation’ i.e.,

more hits on Google.

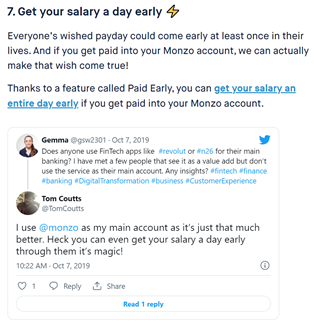

Monzo

If a consumer banks with Monzo, they will receive their salary a day early. This ‘innovation’ has no direct economic benefit: the consumer is not wealthier in the long run, and it is difficult to argue that being paid a day early will materially impact their

well-being. But, as Figure 1 shows, this gives Monzo users the ability to ‘brag’ about getting paid early, which generates ‘word-of-mouth’ advertising for the brand. It also fits into Monzo’s ‘seamless’ digital experience: the consumer can opt in with a single

click. It is easy to imagine a challenger banks’ product development team asking the following questions when they evaluate business cases:

- Will this new product create an opportunity for our marketing team?

- Will our existing customers want to show off the new product to their friends?

To illustrate the success of grassroots marketing techniques, in Monzo’s 2021 Annual Report they noted that 92% of the growth in their five million strong customer base was through ‘organic’, word-of-mouth growth(6).

Figure 1 – Monzo’s ‘Get your salary a day early’ scheme(2).

![]()

Challenger banks show a greater awareness of consumer trends.

Starling Bank

In 2020, Starling Bank became the first UK bank to make their debit card out of recycled plastic(8). This is because many consumers want to shop for (or in this case with!) products that are environmentally friendly. This was a simple, but effective, way

to show that Starling Bank cares about the same problems as their customers do. Whilst most traditional banks were just talking about becoming ‘greener’, Starling Bank prioritised a project that put their commitment to supporting the environment straight into

the hands of their customers.

Traditional banks also under-value revenue from advertising and marketing partnerships.

Revolut

Revolut runs a programme, ‘Revolut Rewards’ that offers discounts and cashback offers to all customers with a current account by partnering with retailers. The discounts are tailored to each individual, using information from the customers purchase history;

it is therefore a seamless, digital, personalised marketing tool. Santander’s ‘Retailer Offers’ is offered to all current account holders, but is harder to find in their mobile app (than on the Revolut app) and the rewards are not personalised. This could

be because Santander has not prioritised the right kind of projects to optimise their rewards programme for the digital era.

The examples given for Monzo, Revolut and Starling, show how challenger banks have been able to promote their brands by:

- Enabling products that support marketing schemes;

- Prioritising projects that show empathy towards consumer’s issues;

- Personalising products for their customers.

These innovations have contributed to challenger banks obtaining 14% of the market share for the UKs primary account switching service, as of 2021(3). This is largely one way traffic, for example, Starling Bank saw 17 customers switch to them for every (one)

customer that left(7). Much of this switching has come at the expense of the UKs traditional high-street banks. If the traditional banks wish to stop customers moving to the challenger banks, they will need to develop more digitalisation business cases and

update their evaluation methodologies to better support their digitalisation strategy.

Obstacles for Traditional Banks

So why are traditional banks currently unable to prioritise the same business cases as the challenger banks?

One possible explanation is an inability to financially model the indirect benefits associated with digital change, for example by underestimating revenue from partnerships with online retailers. Therefore, enhancements to digital infrastructure fall

behind ‘standard’ changes when banks prioritise projects.

Another reason could be that traditional banks do not have the right stakeholders

sponsoring projects. In traditional banks, the typical project sponsor is a ‘head of’ an established banking function. In the challenger banks, project sponsorship is more likely to come from stakeholders who do not have a background in financial services.

For example, Monzo’s Chief Product Officer spent five years working in in ‘ad and consumer products’ at Facebook(5). This representation at a senior level keeps digital strategies high on the agenda for the challenger banks. They, and their subordinates, can

act as digital translators for the traditional financial departments of the firm. As such, projects that prioritise effective digital strategies are typically implemented quickly and successfully.

Furthermore, traditional banks may be held back by legacy internal systems, such as ‘green-screen’ core banking applications, shown in Figure 2, that use outdated coding languages (such as COBOL). As such, traditional banks suffer from higher costs

associated with integrating digital services and legacy infrastructure. In turn, this increases the cost associated with digital projects compared to other transformation projects. Prioritising overhauls of core-banking applications, by enabling API technology

or replacing them entirely, is a ‘gateway’ change that will enable traditional banks to improve their customer offering.

Figure 2 – An Example of a 'Green-Screen’ Application

![]()

Strengthening Partnerships with Fin-Techs

Once banks have upgraded their legacy infrastructure, one of the ways they will be able to improve their digitalisation initiatives is through fin-tech partnerships. Returning to the previous example of retailer partnerships, Monzo partner with Tail, a fin-tech

that offers cashback and discounts. Tail can be accessed through the Monzo app, via APIs, enabling Monzo to add another revenue stream without a large investment. Enhancing API technology would enable traditional banks to compete with the

plug and play technology that challenger banks already offer.

Fin-techs can also provide benchmarks for performance in the banking sector, even in the areas still exclusively dominated by traditional banks, such as the mortgage market. Consider Trussle, the winner of the “UK’s Best Mortgage Broker” at the 2021 UK British

Bank Awards. Trussle offer a ‘Speed Promise’ which guarantees mortgage advice within 24 hours and a mortgage offer within five days. Only 5 of the 90 mortgage providers available through their brokerage service can turn around an offer in this timeframe. This

is much faster than the average response time from banks of 24 days(9).

There are currently £1.6 trillion worth of residential loans in the UK mortgage market(4). If traditional banks are slow to review their mortgage processes, like they have been in the market for current accounts, there will be a huge shift in revenue from

established financial institutions to the challenger banks. By tracking performance benchmarks set by leading fin-tech institutions, such as Trussle, traditional banks can effectively prioritise projects and stay ahead of the game.

Conclusion

In the future, we will see traditional banks continue to try and emulate the digital strategies of the up-and-coming challenger banks. To do this, traditional banks will need to improve the methodologies they use to prioritise and deliver digital products

and services. They can do this by considering whether a project will: support marketing schemes, show empathy towards customer’s issues and speed up or personalise the customer experience.

The key factors that will allow banks to do this are: upgrading legacy core-banking systems and hiring more ‘digital-translators’. This will unshackle banks from legacy technology restrictions and encourage a better appreciation of the indirect benefits

of digital projects. In turn, this will help improve the modelling of business cases, as digital product enablement ‘know-how’ is embedded into traditional banks’ transformation teams. This can help improve traditional banks’ digital experiences and unlock

new avenues for growth, through partnerships with fin-techs and other digital channels.

Finally, traditional banks can monitor performance benchmarks set by influential fin-tech providers to ensure that their products remain relevant in the digital era.

For more information on how Be UK can help you navigate the challenges of banking in the digital era, please get in touch!

Bibliography

- Bank of England. (2021). How could the recent increase in homeworking affect the economy? Retrieved January 8, 2022, from https://www.bankofengland.co.uk/bank-overground/2021/how-could-the-recent-increase-in-homeworking-affect-the-economy

- Borbon, B. (2019). 10 Magical Monzo Features. Retrieved January 12, 2022, from https://monzo.com/blog/10-magical-monzo-features

- CASS Switching Service. (2021). CASS Switching. Retrieved Jan 8, 2022, from https://www.bacs.co.uk/

- FCA. (2021). Mortgage lending statistics - December 2021 . Retrieved January 14, 2022, from https://www.fca.org.uk/data/mortgage-lending-statistics

- Hudack, M. (2022). mhudack. Retrieved January 8, 2022, from https://www.linkedin.com/in/mhudack/

- Monzo. (2022). Year in Review. Retrieved January 15, 2022, from https://monzo.com/annual-report/2021/

- Norrestad, F. (2021). Current account switches of United Kingdom (UK) banks Q2 2021, by net gain/loss. Retrieved January 13, 2022, from https://www.statista.com/statistics/417599/current-account-switching-by-bank-gain-or-loss-uk/

- Starling Bank. (2022). PERSONAL CURRENT ACCOUNT. Retrieved Jan 16, 2022, from https://www.starlingbank.com/current-account/

- Trussle Lab Ltd. (2022). Trussle's Speed Promise. Retrieved January 9, 2022, from https://trussle.com/about-us/speed-promise