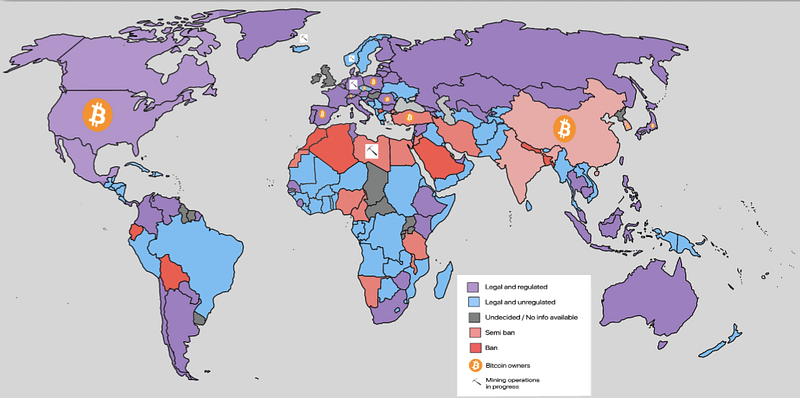

Bitcoin, blockchain, crypto, regulations, governments, bans, unworthy, revolutionary, so many news articles on the topics, none with any real worldwide summary.

Each country reacts differently to bitcoin and its technology. The blockchain here is a little résumé of what is currently happening when governments face bitcoin.

The fearful ones: Turkey, India and China

Turkey, India and China are some of the countries that even though they are intrigued by cryptocurrencies they are also scared of it.

Turkey decided a few weeks ago to ban the use of cryptocurrency as a payment method due to its

lack of regulation and possible losses due to the exchange rate. The consequence of this action is to label cryptocurrencies only for trading and investment purposes, and not general payment use.

Crypto trading volumes in Turkey hit 218 billion lira ($27 billion) from early February to March,

up from just over 7 billion lira in the same period a year earlier, furthermore, trading spiked in the days after Erdogan replaced the bank governor, sending the lira down as much as 15%. This could have been seen as cryptocurrencies being a potential threat

to their currency and a fear of losing control sealing the ban decision.

India has not yet banned crypto although they have voiced a proposition to do so, multiple times, which is intriguing when results showed that over

$2 billion have been traded on Indian crypto exchanges and this in one month. This ban could be the result of the governments being worried about the fast-growing popularity of crypto trading.

Nischal Shetty, CEO of WazirX a crypto exchange based in India posted the trading volume of his exchange and in 2 months it went from an unknown platform to a

leading Indian exchange, now struggling to keep up. The speculative situation and the lack of control over it, bearing in mind that India raised an SOS to the world a few days ago, makes crypto a method to send money away from the country when it needs

capital most.

Still, this proposition does not worry the big exchanges like Coinbase who are on a hiring

spree in India.

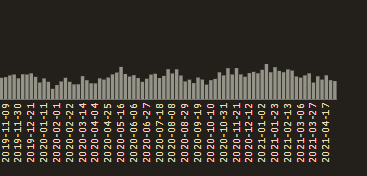

China is different from the other two countries. Gray (or half red on the map) is definitely its colour. In 2017, ICOs were completely banned and numerous companies shut down or moved. However, when looking at the map and activities, it is clear that P2P

crypto trading still occurs within China.

Above the volume bar chart is the P2P activity within China for the

last 2 years that we know of which is remaining steady. Many more small local P2P traders are also active that go unadvertised within China.

Officially crypto is not banned, but the country has made it very hard to do any large scale crypto business there. Big exchanges like Binance, the largest exchange in the world moved out of China and adopted the use of stablecoins like USDT and enjoys a

large lead which net-net is a big loss for China.

In the struggle to stay ahead in the financial industry, China has pushed hard on the

CBDC front and is experimenting with public blockchain stablecoins

offshore in Labuan.

There are other countries that seem to be in the rush towards blockchain and decentralised finance. In one article, a representative from ISTANEX, a Turkish crypto provider, resumed the situation

in the Middle East and in the rest of the world regarding the digital currency, explaining that a lot of these countries actually fear the digital yuan but the risks may be overstated due to the CNY’s low volume at barely 5% use within global trade.

Still, these countries fear crypto as they compete with their already fragile economies.

The Curious ones: the UK and the EU

Meanwhile, in the EU and UK, the noise created by the blockchain is making these governments curious yet cautious. Located right in the middle between the US rules and China’s ban, these countries are conflicted in how to best regulate cryptocurrencies.

Instead of treating them like a currency, they impose heavy tax rendering them more like a stock or other investments, despite the crypto also being used as a currency.

The UK harbours its pride to encourage innovative financial services and crypto startups, but on the other hand, some of its leaders are making sweeping contradictory statements: Andrew Bailey, governor from the Bank of England warned cryptocurrency investors

to “be prepared to lose all your

money”.

In Europe the rise of crypto acceptance is noticeable. In 2018, it was found that only 7% of the French

people had cryptocurrencies which correspond to a slow start. Although France kept the pace up in the last 2 years and the final acceptance was seen when the French Economy Minister Bruno Le Maire offered to its European counterparts the establishment

of a single regulatory framework for crypto-assets starting by creating the Paris Blockchain Week in order to give France the status of the crypto-nation. Around France, Italy and Spain have already allowed crypto, although do not recognise their legal tender

status qualifying cryptocurrencies as means of exchange, different from e-money by the regulators.

A very similar rise happened in the UK where the number of people who have bought crypto has increased by

558% since 2018 when just 3% of the population owned cryptocurrency before.

Some weeks ago, Rishi Sunak, the English chancellor announced the creation

of a top-level task force to explore the benefits and risks of a Bank of England digital currency for the UK which could possibly be named Britcoin.

However, the Financial Conduct Authority issued a warning to would-be investors in January, saying consumers should be prepared to lose all their money if they invest in schemes promising high returns from digital currencies like bitcoin. That particular

announcement concurred closely with the UK Asset Manager Baillie Gifford investing about $100M in Blockchain.com,

interesting it is.

It is safe to say that the EU and the UK are still in the discovery stage when it comes to crypto yet still trying to establish new financial technologies such as Bitcoin as a kind of middleware technology that can work between traditional currencies and

cryptocurrencies.

The Adaptive ones: South Korea and the US

The United States, the land where anything is possible but at the same time not. As soon as crypto appeared and made waves about its use, the US accepted it and developed it and has a vicious body to control it: the SEC.

The SEC is known for being slow but meticulous. Once a crypto company is on their radar you can be sure no stone will go unturned. Case-in-point, Ripple Labs

has been in court against them for months and with no clear decision about their right to resume their activity or not.

Despite the use of contradictory regulatory environments, the US can still be considered the country with the most crypto businesses and the largest for that matter, and with the looming potential for not just a Bitcoin ETF but also an

Ethereum ETF, the US has a chance to prove its adaptiveness.

South Korea, is known to be one of the most advanced countries in the world and it is only natural that crypto adoption would take off. Unfortunately, recent regulatory events could put a stain on the tech-forward image.

Due to capital controls, there are crypto price premiums for buying and selling cryptocurrencies within Korea, this has led to even more trading activity which has triggered a number of regulatory announcements on crypto tax for 2022.

Crackdown headlines begin propping up in a bid to tame the markets. Just a few weeks ago the city government of Seoul seized

$22 million in cryptocurrencies from individuals hiding their crypto assets on various exchanges. More than a thousand individuals were identified as tax evaders in South Korea, inputting into question the country’s crypto tax heaven image.

Nevertheless, crypto is still on the rise in Korea and the government hasn’t given any evidence of a blanket ban or any strong stance as of yet.

The only seemingly big regulation imposed on crypto has been on allowing automated bank deposit and withdrawals which are only given to a few select few older exchanges, and although these automated payments do create an unfair competitive edge to the select

exchanges that have them, it still gives crypto companies within the country something to strive for, especially the earliest and most experienced crypto businesses.

HollaEx is an example of an early South Korean company, founded by an international team that operates largely remotely, a key value of the cryptoverse. Established for over 5 years, the Korean crypto service provider

offers white-label crypto exchange software that allows for crypto-asset creation, exchange and wallet technologies to other businesses wanting to connect crypto into their existing business.

It is no wonder that South Korea is attracting

global crypto talent as a country with the 4th most patents and playing an increasingly critical role in chip manufacturing and now

the regularly

top crypto trading volume in the world, South Korea could easily evolve into a crypto powerhouse.

Parallel economies: Africa and South America

These emerging countries could be renamed the ‘smart ones’ as they are using stablecoins (USDT, USDC etc) to avoid the exchange rate inflation from their national currencies.

These countries’ inhabitants are often unbanked and crypto is the best and at times only solution to do international business payments and safeguard against runaway inflation.

One such example is the Brazilan platform called Moeda who facilitates access to financing to local communities, and they offer crypto technical support to businesses. This saves small businesses from going through a traditional financial intermediary and

instead finds financing directly sourced through cryptocurrencies within the Moeda system.

Fact: Moeda is utilizing the HollaEx Kit as their go-to crypto tool kit. The kit helps anyone to deploy their own crypto platform, coins and is the technology used in the live demonstration of their

crypto exchange deployment.

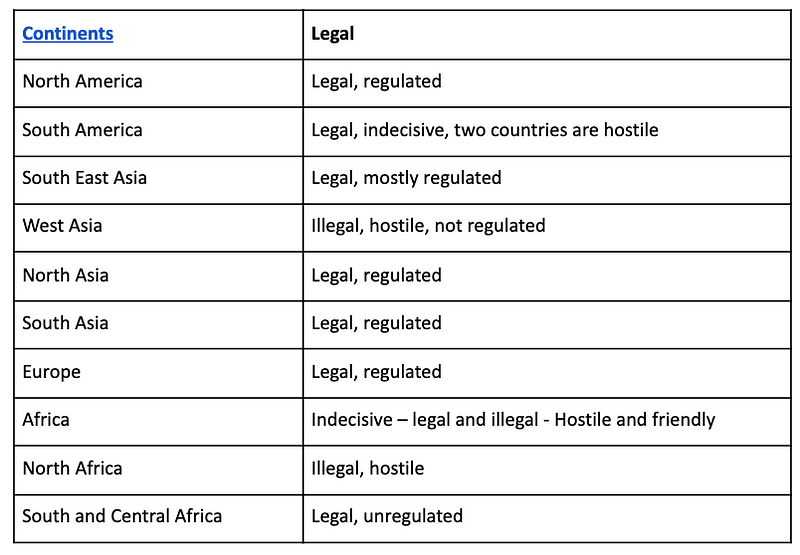

Crypto legal status by continents

The Pressures on for Governments

In summary, there is still a real lack of knowledge around crypto, and

governments are not really in the game to explain cryptocurrencies. Instead many countries seem to be slowing down adoption by portraying crypto assets as extremely risky and that extra protective measures are necessary in order to use them.

How much regulation to apply is the big ongoing debate in 2021 as prices are attracting a new wave of cryptocurrency users.

The truth is crypto at its core is quite easy to understand and has the potential to do good for a country’s populace if only as an

inflation hedging tool. But the real potential for crypto technology is in its leapfrog capabilities, where emerging countries can simply skip banking infrastructure and go straight to using public cryptocurrency blockchain infrastructure instead.

And there is big evidence that countries are indeed

skipping banking infrastructure which will most likely push the world into a sort of cryptocurrency age. Some countries are even starting to

integrate crypto mining within their nation planning and creating tax break incentives which is the case for the small ex-soviet country of

Georgia.

However, the reaction of certain countries is showing a potential weakness of their economies. An interesting fact is that both China and South Korea limit foreigners from participating in local crypto trading on their platforms, whereas western platforms

like Kraken span operations globally. This shows a certain hesitation by some Asian nations to open their economies to the world in fear of capital flight. For example, China or even South Korea are continually grappling with capital controls which makes regulating

crypto difficult as fears of another

Asian financial crisis was not that long ago in the memories of these countries.

Chinese President about crypto (Source)

While already diverse countries like the US and some European countries are steadily weaving the technology into their already existing financial system through digital asset exchanges, sophisticated crypto custody and the rise of CBDCs, it is only a matter

of time that a crypto account will be provided within all western

retail bank accounts.

Whatever countries do with their crypto regulation one thing is sure, there will always be another country ready to provide crypto investors, traders and businesses the incentives to do business within their country instead which we see with

Portugal and smaller island nations.

A light touch to regulation seems to be the only path forward or miss out on the gains from what could possibly be the next base

financial infrastructure

of tomorrow.