The main reason to switch is that ISO 20022 payments messages carry much richer information than the redundant SWIFT MT messages and other legacy formats commonly used today.

Also, the information in an ISO 20022 message can be grouped together based on common data components from different payment methods and can be further reused, resulting in increased interoperability. This attribute of ISO 20022 relates not only to interoperable

routing of domestic and cross-border payments but also across different types such as ACH, real-time and high-value payments.

How Can Data Transform The Ecosystem?

1. Data enables more types of payments

The ability of data to move along with payment is enabling more types of payments. Request to Pay or Request for Payment (R2P) is a perfect example of a payment type enabled by data.

The value of R2P is that the requestor can raise the obligation to pay and include all the necessary information about the payment in a message that travels to the recipient electronically. The recipient then has all the information they need to initiate a

payment, and all the un-altered information travels back with the payment for use by the requestor.

R2P enables financial institutions to offer a smarter payment collection capability to several customer segments, saving them time and money compared to their existing process.

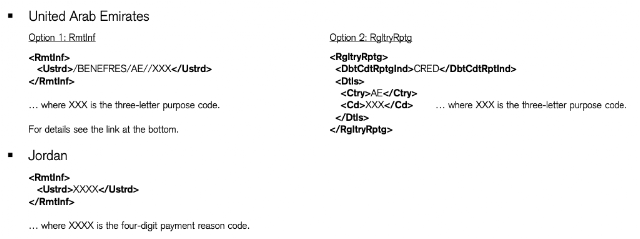

Illustration of Regulatory Reporting Requirements

2. Data Facilitates Reconciliation And Enhances Fraud Detection

Historically, the lack of contextual information associated with payments could make reconciliation more difficult and error-prone. A simple refund payment lacked the ability to convey this detail, and could be credited to an account with no context whatsoever.

With ISO 20022, data-rich information can travel along with the payment and be tracked using gpi. Payments now also carry more structured data and include information about the parties involved in the transaction. This data can be communicated in a streamlined

way, across borders.

3. Payment Data Is The Most Critical Component In The Area Of Sanctions Screening

Even when the payment itself offers little insight, the data provided the raw material to help reduce risk and combat fraud and financial crime. As machine learning (ML) and artificial intelligence (AI) become more prevalent, the ability to accurately analyze

payments data grow, leading to more refined insights that will enable better and quicker decisions and enhance fraud detection. The ability to track transactions and spend patterns in real-time will also allow for effective and efficient fraud mitigation and

prevention while minimizing disruption to customers' business.

A growing volume of payment data will continue to unlock new revenue streams and business opportunities as companies turn information into valuable insights to inform business strategy, improve customer experience, and minimize risk.

Illustration of API connectivity

4. Standardized API’s

Messaging standards are published centrally, with a comprehensive review process that leads to an annual update. By contrast, API development is done in a much more agile and decentralized manner, where it is designed, developed, and validated by the application

owner as a part of the application development cycle. The nature and structure of API call now largely depend on the internal data model chosen by the application designer as well as the business processes implemented.

ISO 20022 will foster standardization at the industry level to reuse the data dictionary thereby simplifying the task of integrating the API to existing financial systems and processes.

5. Open Banking

API standardization is important if open banking initiatives are to deliver on their promise of improved efficiency and fair competition. Without it, each bank must design its own implementation, leading to a great burden of complexity, risk, and cost for

anyone seeking to create value by aggregating services from multiple banks. Standards are also important to ensure that APIs capture data that is compatible with back-office and downstream processes, otherwise the risk increases where that data will be misinterpreted

or corrupted as it flows through the financial system.

The ISO 20022 technical community has also worked to evolve the standard to accommodate API community. These evolutions include adding a JSON notation for ISO 20022 at the physical level, adding support for state models at the logical level, and designing

a "fast track" registration process more appropriate to agile API development and publication cycles.

Illustration of Centralised and Decentralised system

6. Distributed Ledger Technology

As DLT matures it is clear that DLT may not replace banks’ back-office systems, but will integrate with existing back-office technology using APIs. It opens an avenue to explore the usage of ISO 20022 business definitions.

In summarization, the migration to ISO 20022 involves a degree of complexity and challenge far beyond any technological transformation and yes all of the benefits outlined come with a price tag. But it will ultimately offer banks the opportunity to re-evaluate

their business models and market positioning, as well as finally get their infrastructures ready for the digital future of payments.