The world will never be the same again - regardless of when and under what conditions Brexit will actually happen (and whether it will happen at all): certain things, including the financial world, will never go back to the way they were.

First and foremost, financial companies with British licenses have realized the risk of losing authorization to provide financial services within the European Union (EU): once the UK leaves the European Union (EU), theoretically, financial companies will have

to give up their non-UK customers. And yes, a smooth transition period is also be possible here, but the risk of disconnecting from SEPA payments and the chance of losing the entire European audience does not sound very encouraging. Both financial companies

(they keep an eye on new jurisdictions) and European clients start to think about any potential impact from Brexit, when choosing their payment institutions. Today, “what would happen to me in the event of Brexit” is one of the most frequent questions from

clients opening an account with payment institutions with a British license.

Supported by a relevant series of numbers and graphs, we make suppositions about the perspectives of how this affects the geography of fintech.

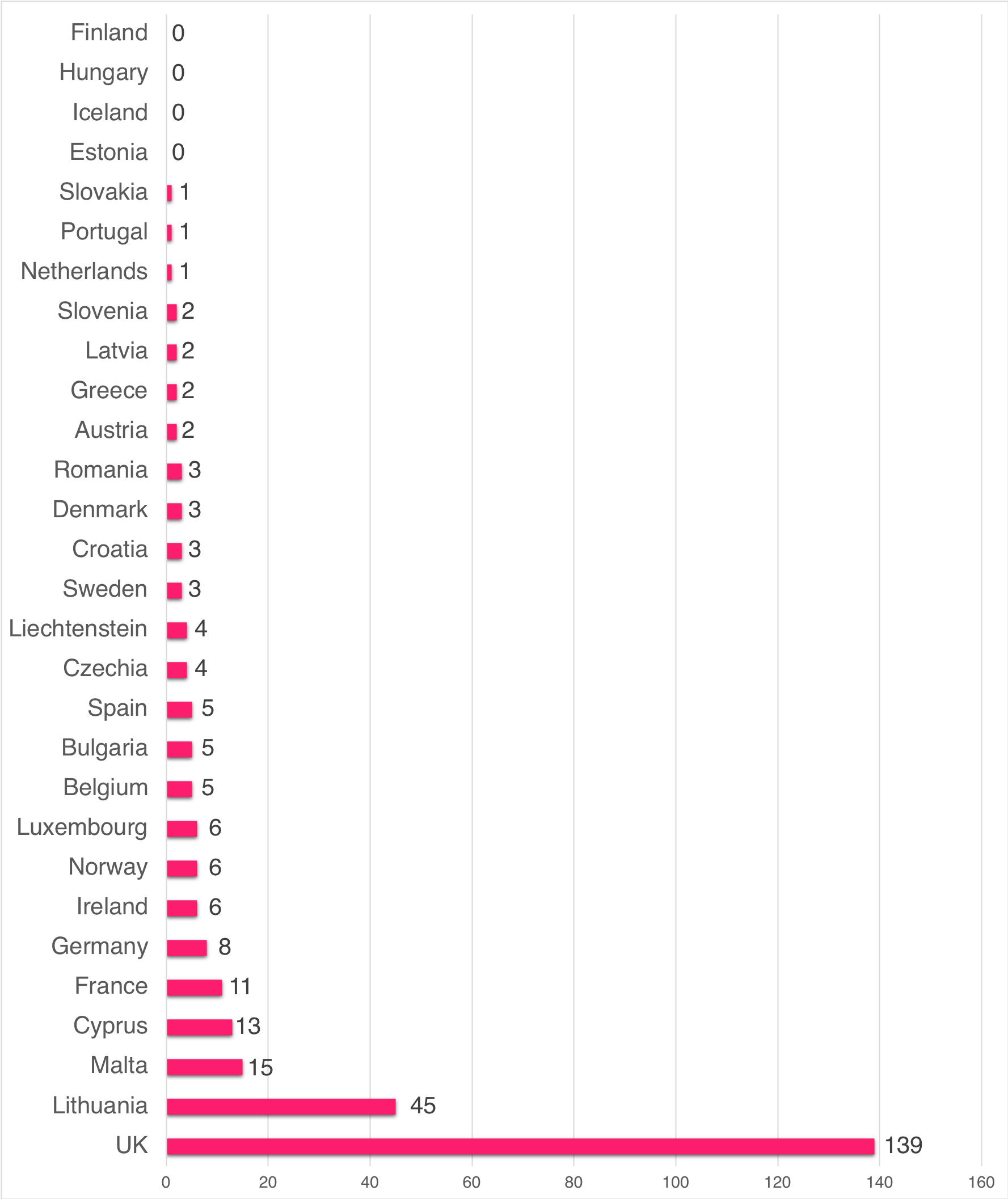

Number of EMI licenses granted by countries (until March 2019)

Now let's look at the example. Together with my colleagues at Bilderlings, we studied statistics of regulators for countries in the European Economic Area (EEA) in regard to how many Electronic Money Institution (EMI) licenses each country has issued to

the present day*. The EMI license is one of the most recognized licenses that fintech companies can obtain: many payment services, electronic wallets and so-called digital banks (or non-bank financial institutions) conduct business, holding the license for

operations with electronic money.

From the chart we can see: the largest piece, almost half of all European payment services are based in the UK (139 licenses). It is followed by Lithuania (51 licenses) and only then - Malta (15 licenses). It is important to pay attention how EMI licenses

are “distributed” across countries: more than 60% of all EMI licenses in Europe are clustered in the UK and Lithuania. And 40% are more or less evenly distributed among other 29 EEA countries (on average, each jurisdiction represents 2% of the total number

of European EMI). The idea is clear with the UK: London is considered as a European financial centre and the capital of European Fintech. But where does Lithuania come from? We will answer this question later, but for now let's take a closer look at other

indicators.

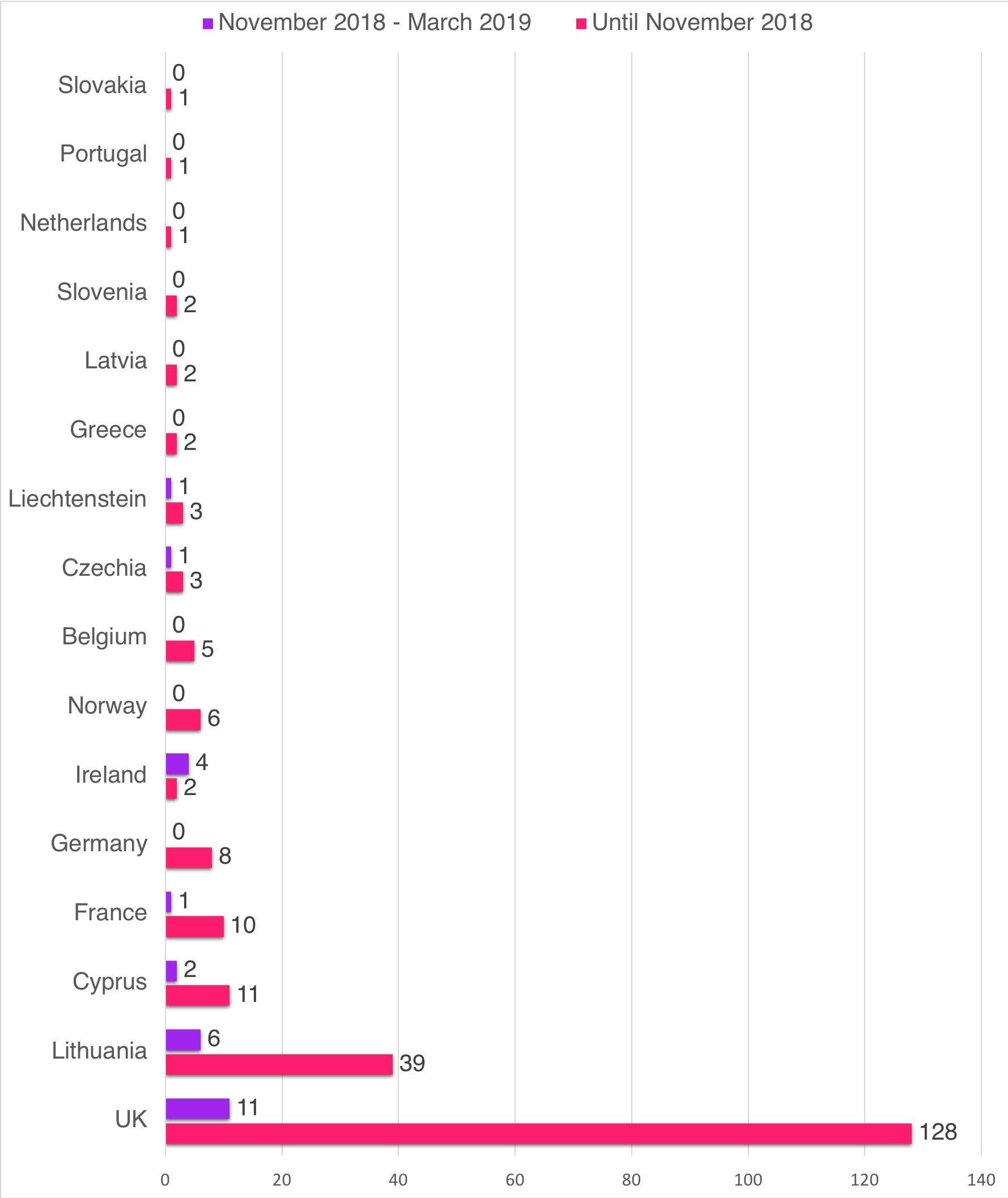

What we really need to do is to take a step back and look at the statistics from six months ago.

For example, in November 2018, 39 companies with an EMI license were opened in Lithuania. According to the source, a little more than a year ago, in February 2018, there were only 27 licenses in Lithuania. To repeat: a small Baltic country in six months managed

to issue 6 licenses and as many as 18 licenses – in a year. That said, over the course of one year the country managed to issue more licenses than the next country on the list - Cyprus (compared to the total number of licenses in Cyprus).

Changes of number of EMI licenses granted by countries (until November 2018; November 2018 - March 2019)

If you want to get a big picture, there is a chart showing how the number of EMI licenses has changed in the period of six months.

If you browse the reports of the Lithuanian regulator, you can recognize how diverse the audience, holding licenses issued in Lithuanian for non-limited activities, look. Among them are IT giant Google, fintech startup Revolut, several other well-known payment

services, as well as companies that do not even have their own website. The geography of the “Lithuanian Fintech” is also varied – there are companies originally from Turkey, Greece, the Netherlands, Iceland and, of course, the owners of the British FCA licenses.

It seems that Lithuania has opened its doors to all comers.

Let us go back to the question - why Lithuania? The answer is: the efforts by the Lithuanian regulator to offer more favourable conditions (much faster and cheaper than in other countries) and also thanks to public statements by politicians and the role

of public relations and the media.

Lithuanian politicians speak with pride that they are ready to become the new capital of Fintech. The member of the board of the Central Bank of Lithuania, Marius Jurgilas told international news agency Agence France-Presse that the financial technology

industry in Lithuania now ranks second after the UK in terms of the number of companies: according to Jurgilas, more than 110 companies have obtained licenses, and 61 applications are being considered. Jurgilas also underlines that Lithuania expects at least

100 applications this year.

Similar statements were also made by representatives of other countries. In particular, Dublin is frequently referred to as "second London" in the media, when discussing the readiness of Ireland to welcome financial companies running away from London. On

the one hand, this is, of course, political PR and big words. On the other hand, Fintech needs to secure a European area, when obtaining a license in countries that have not yet declared their desire to leave the European Union.

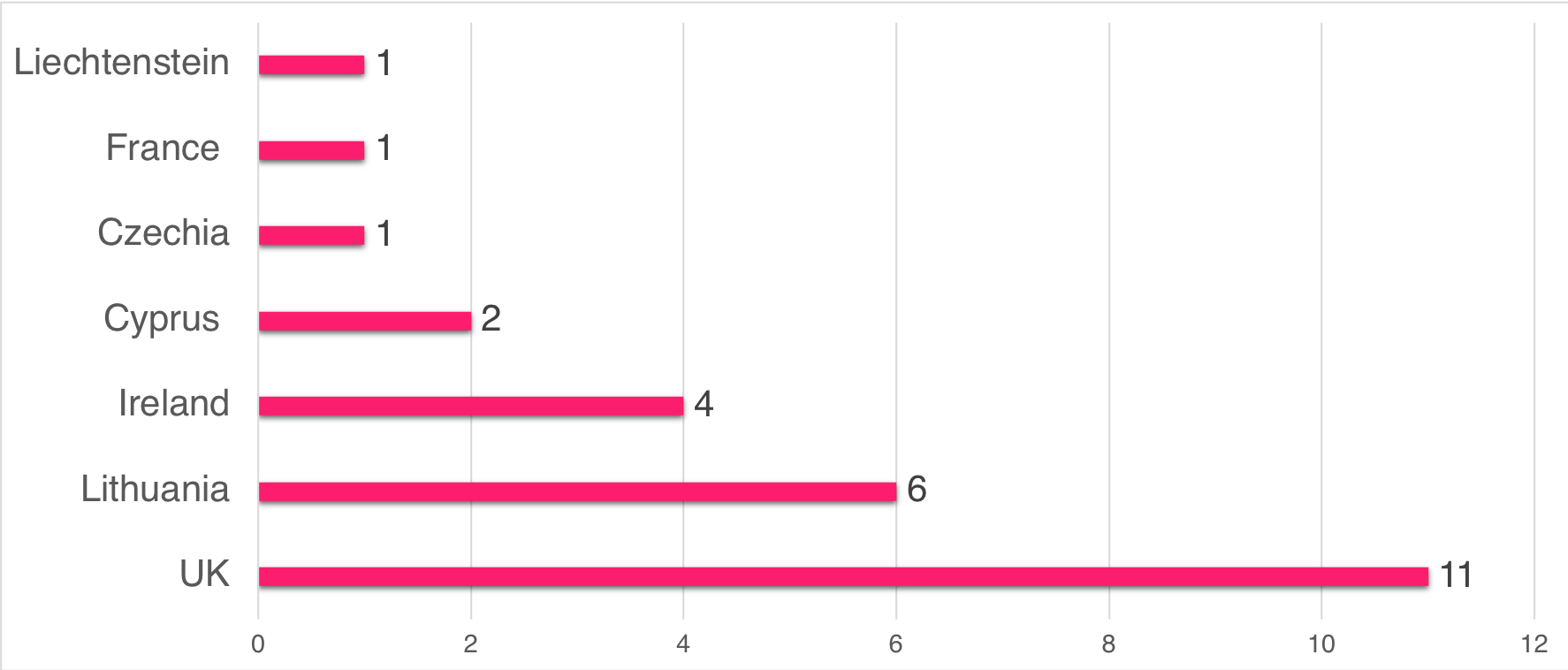

Number of new EMI licenses granted (November 2018 - March 2019)

We should also examine figures and countries, which, beside Lithuania, were actively engaged in issuance of EMI licenses. This is how the chart with half-year figures looks like - which countries have registered the majority of all EMI licenses in the last

six months.

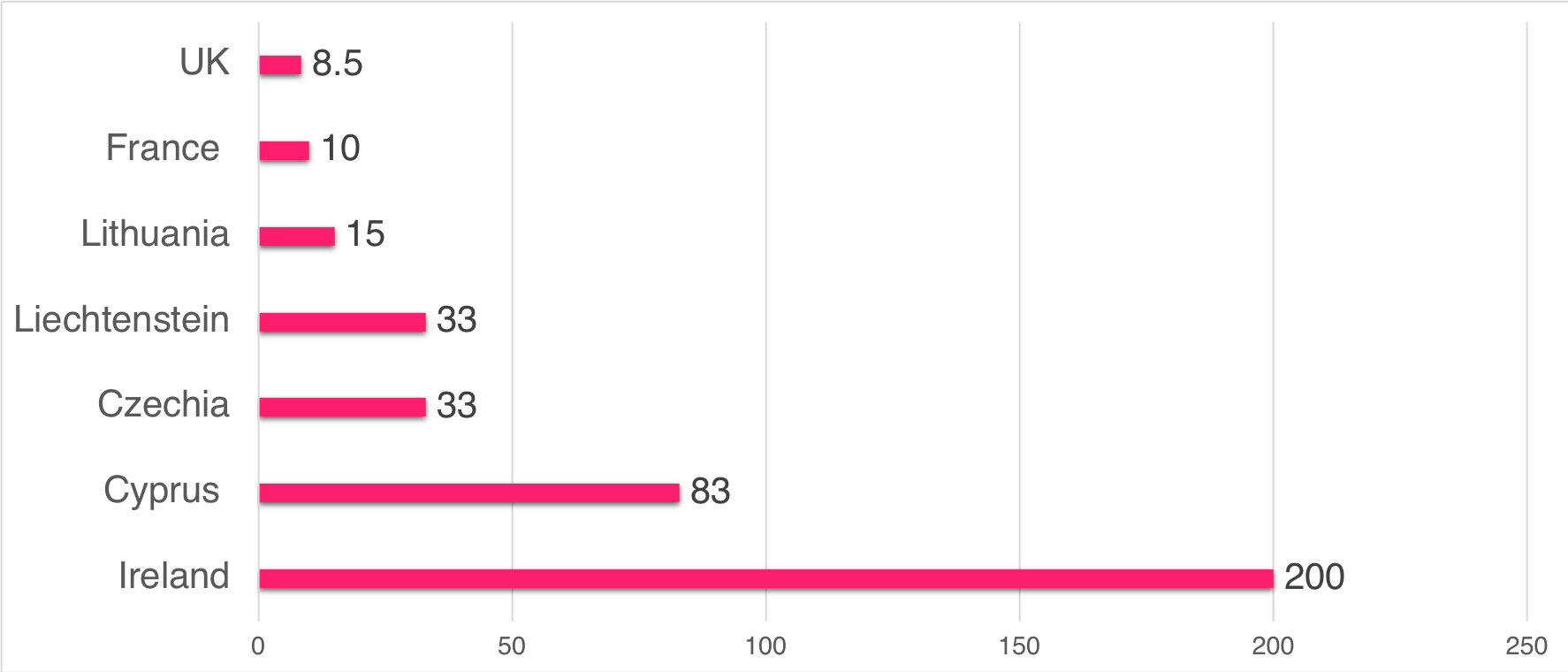

Percentage of EMI licenses granted (November 2018 - March 2019)

And the same chart looks very different if viewed as a percentage of the total. For example, Ireland issued only 4 new licenses over the last year. But if you look at the percentage of the total number of licenses issued six months ago (and even a year!),

it is a 200% increase. Cyprus is the second in the ranking, increasing the number of EMI licenses by 83% in the last six months. And if you examine the yearly figures, EMI increased by 116% over the last year. Other countries rank as follows - the Czech Republic

(33%), Lithuania (15%), France (10%) and the UK with 11 licenses that account for only 8.5%.

What conclusions can be drawn?

If you are struck by the fintech industry and planning to obtain an EMI license in one of the European countries, then Lithuania, the Czech Republic and Cyprus are far more welcoming and supportive than others. We do not have the exact figures for Malta

for the year 2018, but if we trust third-party unofficial sources, the current situation in Malta is similar to the one in Cyprus. However, the reputation of the regulators of these countries is not, alas, flawless: Malta and Cyprus are firmly linked with

offshore companies, the Czech Republic is overwhelmed by money laundering scandals, and Lithuania is one of the Baltic countries that today are a red rag for the bull, when it comes to the Anti-Money Laundering (AML) Policy. If you want to get a license from

a regulator with an impeccable reputation - take a look at Ireland. On the one hand, increasing the presence of EMI by 200% in half a year is an indicator of the country’s interest and readiness to work in the industry. On the other hand, only 6 licenses are

an indicator of the extreme selectivity of the regulator.

In general, we can observe that there is a demand for EMI licenses, and this demand will increase in the future. And if we look at the market globally and talk about the terms, as philosophers, then let us remember that every bubble has a habit of bursting.

As a matter of fact - at the worst possible time.

____________________________________________________________________________________

* We used the most up-to-date data published on the websites of the regulators. Also, it should be taken into account that some regulators do not update data automatically. In reality, numbers may differ slightly. In fact, in some countries there may be

more EMI companies than indicated in the chart.

When preparing the article, the data were taken from the official websites of the financial regulators of all jurisdictions, except Italy and Poland - the regulators of these countries seem to do everything possible so that no one finds the information there.

The article also includes the data from the following sources:

https://eba.europa.eu/risk-analysis-and-data/register-of-payment-and-e-money-institutions-under-psd2?fbclid=IwAR2aCZlIktwAxNxgBYJyGD0LVmW-KdtqOqXHZu_GO4oQrIo9IfubdhzsVz0

https://thebanks.eu/articles/electronic-money-institutions-in-Europe

https://www.bankingtech.com/2018/12/psd2-stats-emi-and-pi-licences-in-europe/?fbclid=IwAR2LXJrGRj0mbbGHHByzw9OqLYZVQmu5-5q0MH4MB04cHnKINGw6FM4Tecg