The last few weeks we, payments experts, were excited with news from banks and their contactless innovations, in an urge to promote electronic payments:

- on October 16,

KBC Bank announced its support for Garmin Pay in Belgium

- on October 30,

Rabobank and ABN Amro announced its support for Garmin Pay in The Netherlands

- on October 30,

BNP Paribas Fortis announced its support for Apple Pay in Belgium

Banks are trying hard to convince customer to change their payment habits. Investing in fashionable innovation is part of that deal. They want to drive out cash to rationalise their cost structure of daily banking.

Cash is a bank’s daily banking enemy number 1: it is highly expensive but loved by consumers.

Cash is a commodity for consumers, with a high hidden cost. Result: no bank dares to transfer the full cost to their customers. The only way is to discredit cash towards these consumers.

The sector it doing a lot of effort to achieve this:

- by marketing campaigns to confront consumers with the risk of cash

- by marketing campaigns to convince consumers that electronic payments are convenient

- through lobbying at government institutions to legally enforce a reduction in cash transactions

- by charging higher fees for cash withdrawals

- by pushing new alternative innovative payment methods

Several years ago contactless cards appeared on the market. The Netherlands were first, and Belgium followed more recently. It is the first time since the introduction of chip and PIN that consumers really experienced a change in their way of making a card

payment.

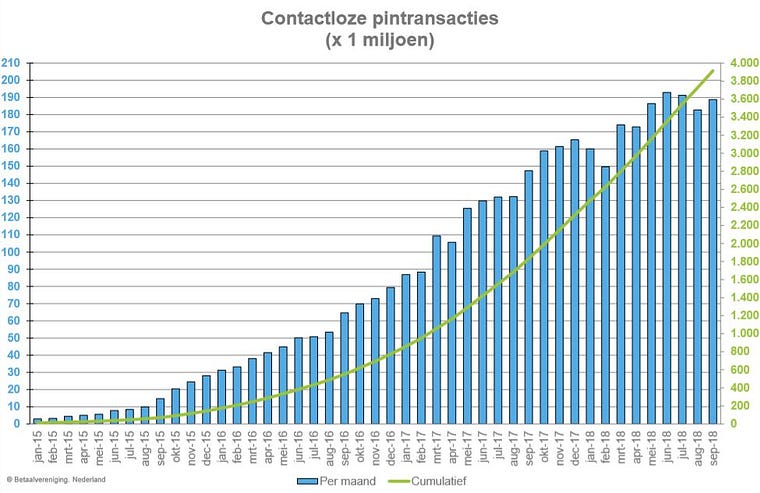

Today contactless cards are a big success in The Netherlands, with

more contactless payments than there are old-fashioned chip-and-pin transactions.

In Belgium things are moving a bit slower. It took many years before the infrastructure was ready on acquiring side. Therefore issuers were not in a hurry to start issuing contactless cards. The classic chicken or egg problem.

Nowadays the industry is trying hard to achieve a similar result. The latest public numbers date from April 2018, when

4% of all card payments were contactless. This is extremely low compared to The Netherlands (+50%), but it is an exponential increase of almost 300% compared to the year before (when only 1,41% of all payments were contactless in Belgium according to the

same source).

Now the acquiring infrastructure is ready, banks are accelerating the issuing of contactless cards. So:

- Chicken: check!

- Egg: check!

Customers still need to get used to the taste of chicken and of eggs. Bancontact is trying hard to help with this through various commercials.

In The Netherlands it took about 3 years for contactless to become a mainstream payment method, after the adoption by the market to issue contactless cards. Transposing this to Belgium would mean that contactless will be the new normal in 2020–2021. All

big banks have switched (at least for their debit cards) and most smaller banks followed this year, if they didn’t already do so before.

Alternatives like contactless wristbands or Apple Pay remain niche. That is exactly why commercials, like the one above, remain necessary to mold consumers for more electronic payments.

Several banks have an Android mobile app that supports NFC-enabled payments (ABN Amro, ING, Rabobank, ASN Bank, Bunq, often

at a cost of 050€/month). iDeal does not support NFC, they only offer the QR-based mobile payment solution.

Contactless wristbands were tested successfully by ABN Amro and Bunq made Apple Pay already available in March this year (2018). No big Dutch bank rolled out Google Pay or Apple Pay thus far.

Belfius is the only Belgian bank today that provides an integrated mobile NFC-enabled payment banking app. Almost all other banks circumvent this by supporting the NFC-enabled

Bancontact app. Both are only available for Android phones of course, with NFC.

Google Pay was made available in Belgium 1 year ago by the 2 biggest banks KBC and BNP Paribas Fortis. Unfortunately, thus far the adoption remains limited. Now also Apple Pay is added on the list at BNP Paribas Fortis, and Garmin Pay at KBC (although this

is, strictly speaking, no mobile solution).

It remains to be seen what the uptake of Garmin Pay will be, given the limited amount of registered compatible Garmin watches: about

20,000 devices for +11 million Belgian citizens. A small calculation shows that 0,18% of the Belgian population can enjoy Garmin Pay IF they are a customer at KBC. With a

market share of about 20% in Belgium, we can assume about 0,18% x 0,20% KBC customers can use Garmin Pay without a lot of effort today. This is 0,04% of the Belgian population. Just to say that looks more like a marketing campaign and a successful demonstration

of KBC’s role as a front runner when it comes to innovation.

The problem with these mobile solutions is the limited acceptance rate: contactless mobile payments are only possible with NFC-enabled Android devices, or through Apple Pay. Garmin Pay can only be accepted by Garmin users… New developments for mobile devices

today are only available to the customers that have exactly that device.

This creates a huge challenge for bank as they need to balance what to invest in: cost vs usage (or press exposure).

I personally think that KBC and BNP Paribas are doing a good job in supporting this kind of initiatives, even if adoption would remain limited. It creates a certain trust in new technologies and it helps consumers to overcome the concerns they still have

on new payment methods. I am convinced this kind of news feeds will also accelerate the adoption of contactless card usage, which is simply more convenient and even safer than regular card payments, despite the messages of organisations like

Test Aankoop. They may be right on the (low) risk that someone can pass your pants with a terminal. But it is so easy to trace back this money, and they can only steal like 25€ (higher value transactions need a PIN).

On the other hand contactless payments allow you to pay for your parking without entering your PIN. You expose your PIN less with contactless cards. As such, contactless cards reduce the risk of skimming: skimmers can still make a copy of your card, but

without the PIN it is a lot less lucrative.

The last few year many new payments methods and devices were created. In the coming years probably many more will follow. On the other hand maybe the biggest change for the near future will be a democratization of the market.

New developments will make it cheaper and easier to integrate new payment means. The payments industry will need to look for hybrid solutions or ‘hubs’ to find the right scale in the future for new payment developments. Maybe PSD2 can be an enabler here,

or solutions like Mastercard’s

MDES.

Interesting times in the world of payments!